Breadcrumb

CalPERS

The California Public Employees' Retirement System (CalPERS) is an agency in the California executive branch that manages pension and health benefits for more than 1.6 million California public employees, retirees, and their families.

We encourage employees enrolled in CalPERS to create an account with my|CalPERS. This will allow employees to view service credit, account balance, view annual statements and keep track of other important account information.

CalPERS Membership

Membership with CalPERS is based on full-time employment for more than six months or half-time employment for more than one year. Lecturers become members at the beginning of their third consecutive quarter at half-time or more, (7.5 units).

Membership is mandatory for qualifying employees. Employees excluded from CalPERS membership are covered by the Part-Time, Seasonal and Temporary Retirement Plan ("PST") administered through SavingsPlus.

You can track your retirement funds and get pension estimates by Creating a MyCalPERS Account.

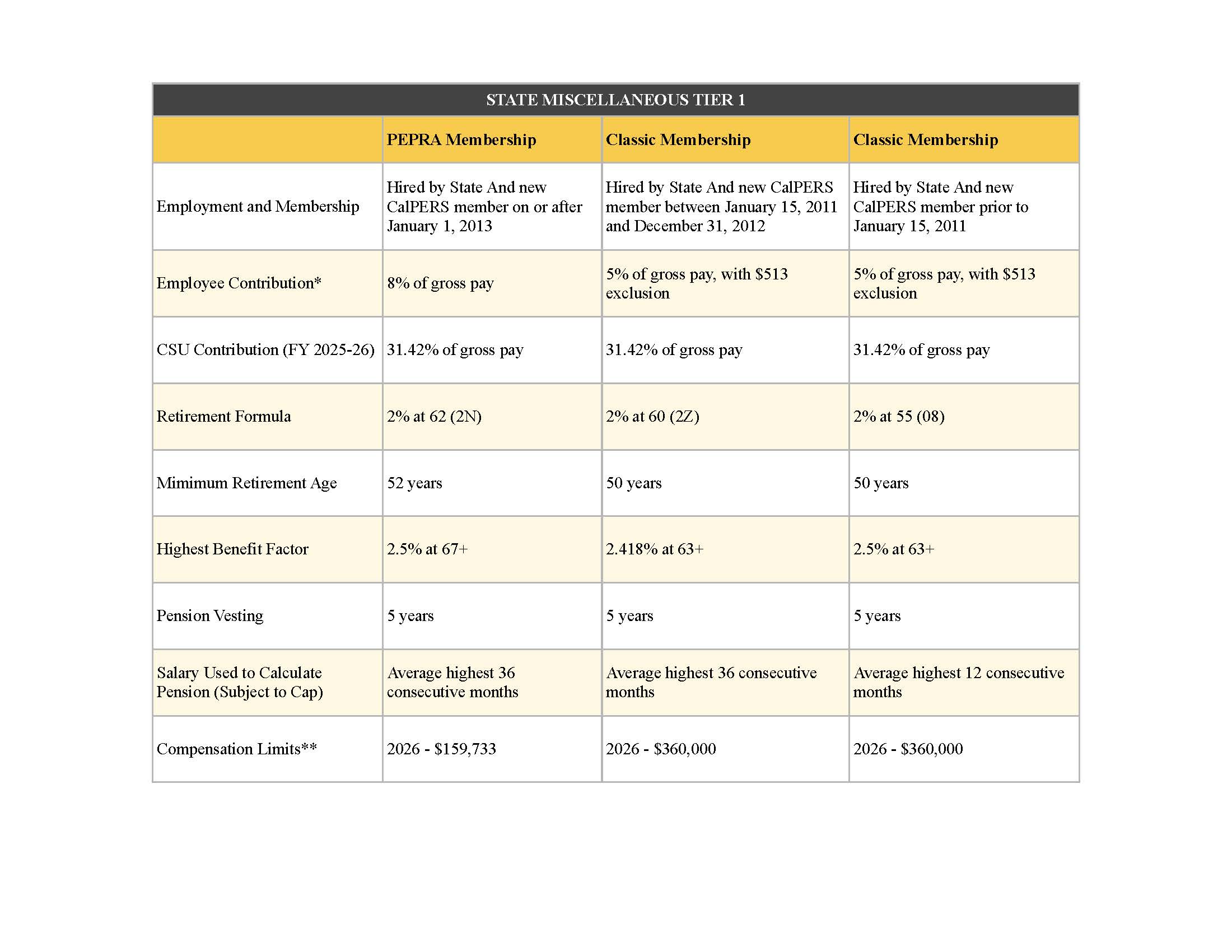

CalPERS is a defined benefit retirement plan. It provides benefits based on members' years of service, age, and highest consecutive 12 months or consecutive 36 months compensation. In addition, benefits are provided for disability, death, and to survivors, or beneficiaries, of eligible members. Note: Some members are subject to Compensation Limits**

Cal Poly Humboldt employees who are CalPERS members become fully vested for a retirement pension after five years of credited CalPERS service. Vesting means you are entitled to a pension once you reach retirement age (varies).

The vesting period is calculated by CalPERS and includes credit earned at any CalPERS public agency including the State of California (including CSU) and public contracting agencies.

You earn service credit for each year, or partial year, you work for a CalPERS covered employer. Service credit is calculated using the fiscal year ( July 1 – June 30).

To earn a full year of service credit during a fiscal year, you must work at least:

- 1,720 hours (hourly employees)

- 215 days (daily employees)

- 10 months full time (monthly employees)

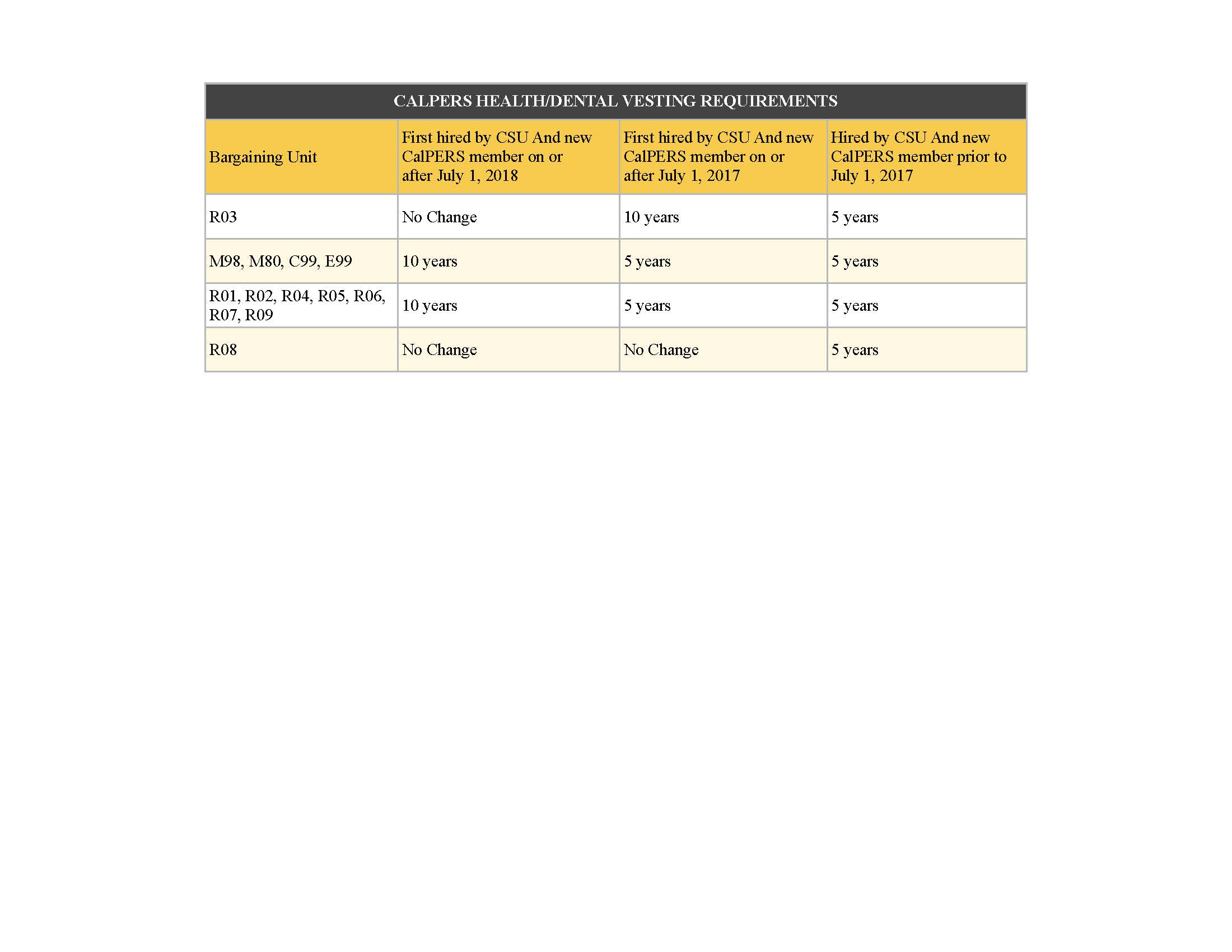

To qualify for health and dental benefits in retirement, you must retire from a benefit eligible position within 120 days of separation from campus AND meet either the five year or ten-year vesting requirement. (see chart below).

- Retirees pay the same health contribution as active CSU employees.

- Dental Retiree Basic plan premium is paid by CalPERS.

- The dental retiree Enhanced Plan can be continued at the retiree’s expense.

- The vision benefit can be continued at the retiree's expense.

In addition, benefits are provided for disability, death, and to survivors, or beneficiaries, of eligible members. Exception to Ten Year Vesting Requirement: Disabled employees would receive the full state health contribution if they separate and retire with a disability retirement within 120 days from a benefits eligible position.

The CalPERS special power of attorney is specifically designed for use by active and retired CalPERS members and beneficiaries. You may already have a power of attorney set up through another resource; however, it may not address your CalPERS retirement benefits.

For more information, please see the CalPERS Special Power of Attorney page: Special Power of Attorney

When you separate from a CalPERS covered employer you have a couple of options on how to handle your CalPERS account.

- Retire:

If you are of the age to retire you can retire with CalPERS and receive your pension, even if you continue working. Keep in mind that once you retire from CalPERS you will not be able to work more than 960 hours in a fiscal year at a CalPERS covered employer. For more information see the CalPERs page on Retired Annuitants.

- Elect a Refund of Contributions:

Receive your accumulated contributions as a direct deposit or rollover. Electing a refund will terminate your CalPERS membership. Ensure you're aware of any tax implications.

- Leave Contributions on Account & Elect to Retire When Eligible:

Leave your accumulated contributions on account until you meet the minimum retirement eligibility requirements.